Financial Regulators Issue Early Warnings Over OneCoin’s Business Model (2015)

As OneCoin’s rapid expansion gathered pace in 2015, financial regulators and consumer protection bodies in several countries began to raise early concerns about the project’s business model.

While OneCoin was still presenting itself as a legitimate cryptocurrency in its growth phase, warning signs were already emerging that set it apart from genuine blockchain-based initiatives.

At the time, global regulators were still grappling with how to oversee cryptocurrencies, a sector evolving faster than most legal frameworks. This regulatory uncertainty created space for projects like OneCoin to operate largely unchecked in their early stages. Even so, by mid to late 2015, authorities in parts of Europe had begun to publicly question whether OneCoin should be trusted.

One of the core issues identified by regulators was OneCoin’s heavy reliance on recruitment rather than demonstrable technological innovation. Consumer watchdogs noted that participation appeared to be driven primarily by the sale of education packages bundled with tokens, rather than by the use of OneCoin as a functional digital currency. This structure raised red flags, as it resembled characteristics commonly associated with pyramid-style schemes rather than financial technology startups.

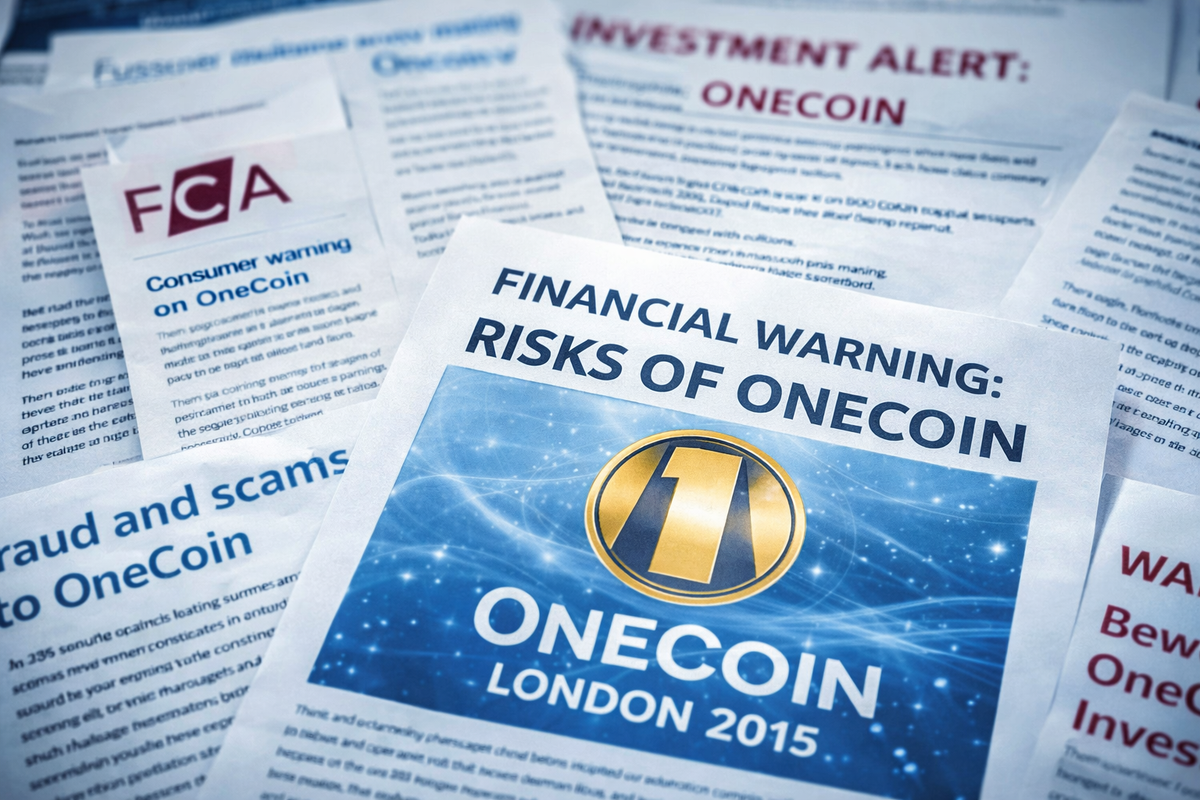

In several European countries, financial authorities issued public advisories cautioning consumers to exercise extreme care before engaging with OneCoin. These warnings emphasized that OneCoin did not operate on a transparent, publicly verifiable blockchain and that its value was determined internally by the company. Regulators stressed that without independent verification, participants had no reliable way to assess the true nature or value of the coins they were acquiring.

Although the United Kingdom’s Financial Conduct Authority (FCA) had not yet taken formal enforcement action in 2015, UK-based financial commentators and consumer advocacy groups also began expressing concern. Analysts highlighted that OneCoin was not authorized or regulated as a financial product in the UK, despite being marketed aggressively to British consumers through events and online promotions. These early observations would later be echoed in broader regulatory actions as investigations deepened in subsequent years.

Globally, regulators faced significant challenges in communicating their warnings effectively. OneCoin’s marketing machine was highly sophisticated, leveraging large-scale events, social proof, and trusted community figures to counter skepticism. Promoters often dismissed regulatory warnings as misunderstandings or as resistance from traditional financial institutions threatened by innovation.

For many participants, these early alerts were either overlooked or misunderstood. Cryptocurrency was still a new and confusing concept for much of the public, and official warnings were often technical in nature. In contrast, OneCoin’s messaging was simple, aspirational, and emotionally compelling, making it more persuasive than cautious regulatory language.

Despite these challenges, the warnings issued in 2015 would later prove prescient. As investigations expanded in the years that followed, regulators and prosecutors would point back to these early concerns as indicators that OneCoin’s structure was fundamentally flawed. Court filings would eventually confirm that OneCoin lacked a real blockchain and that its business model depended heavily on continuous recruitment rather than legitimate economic activity.

By the end of 2015, OneCoin continued to operate and grow despite mounting skepticism. However, the regulatory warnings issued during this period marked the first official acknowledgment that the project posed serious risks to consumers. These early signals would later form the foundation for coordinated international action that ultimately would bring the scheme to an end.